The Role of Public Affairs and Government Relations in International Business Diplomacy

Abstract: Rare earth elements have moved from the margins of industrial policy to the center of global competition, yet many senior executives still treat them as a procurement problem. That is a category error. Rare earth dependency is now a leadership and governance challenge. It requires companies to integrate public affairs and government relations into core strategy, not leave them at the edge of communications or compliance. Drawing on the 2010 China-Japan export disruption, Russia-related sanctions and supply shocks tied to the war in Ukraine, Ukraine’s emerging role in allied critical minerals planning, Iran’s mineral and geopolitical relevance, the revival of Mountain Pass, the EU Critical Raw Materials Act, the Minerals Security Partnership, and Apple’s Daisy recycling system, this article shows how supply chain decisions have become acts of diplomacy. For leaders, the mandate is clear: elevate rare earth and critical minerals risk to the board level, rebuild public affairs as a source of geopolitical intelligence, and align sourcing practices with the resilience, transparency, and sustainability their companies claim to advance.

Key Takeaways for Senior Leaders

For senior executives and board members, the central lesson is clear: rare earth dependency is no longer a technical sourcing challenge that can be delegated to procurement. It is a strategic leadership issue that sits at the intersection of governance, geopolitical risk, public affairs, regulatory strategy, and corporate resilience. The companies best positioned for the next decade will be those that elevate critical minerals exposure to the board agenda, use public affairs as an early-warning and policy-shaping function, and build credible sourcing, recycling, and partnership strategies before the next disruption forces their hand.

- Rare earth dependency is a board-level governance risk. It belongs on the strategic risk agenda alongside cyber, climate, sanctions, and regulatory exposure — not buried in procurement dashboards.

- Current conflicts are turning mineral access into geopolitical leverage. Ukraine, Russia, Iran, and China show how war, sanctions, export controls, and reconstruction finance can reshape supply chains faster than companies can react.

- Public affairs is now a core supply chain capability. Companies need government relations teams that can read geopolitical signals, shape policy, anticipate regulatory shifts, and connect sourcing decisions to national-security priorities.

- Diversification is necessary but not sufficient. Boards must look beyond supplier lists to processing capacity, sanctions exposure, transport routes, traceability, recycling, offtake agreements, and political risk.

- The winners will build credibility before the next shock. Companies that invest now in transparent sourcing, allied partnerships, recycling, and policy engagement will have more options when the next disruption arrives

Rare Earths Are a Leadership Test. Is Your Company Ready?

Rare earth elements rarely appear in earnings calls. They are easy to bury inside procurement dashboards, supplier-risk spreadsheets, or sustainability reports. And until they become unavailable, most executives do not spend much time thinking about them.

That is no longer tenable.

The rare earth question used to belong to procurement. It does not anymore. A company’s supply chain is increasingly a foreign policy decision — and many boards have not yet recognized it.

Rare earth dependency is not simply a materials-management problem. It is a strategic governance imperative. Companies that fail to integrate public affairs and government relations into core business strategy will remain exposed to the geopolitical disruptions, regulatory shifts, sanctions risks, and supply chain vulnerabilities that increasingly determine who can compete — and who cannot — in the rare earth era.

The warning signs have been visible for years. In 2010, during a territorial dispute between China and Japan over islands in the East China Sea, China restricted rare earth exports to Japan. The decision was not made by commodity traders reacting to price signals. It was made by policymakers using resource leverage in a geopolitical dispute. Japanese manufacturers suddenly found themselves scrambling for materials they had barely considered strategic. The disruption was temporary. The lesson was not.1

Fifteen years later, that episode no longer looks like an anomaly. It looks like a preview.

Rare earths and adjacent critical minerals now sit inside some of the world’s hardest geopolitical problems: Russia’s war in Ukraine, sanctions against Moscow, Ukraine’s reconstruction, Iran’s regional and sanctions exposure, China’s export-control strategy, instability in mineral-rich regions, and the growing contest over clean energy and defense supply chains. In this environment, sourcing decisions are not neutral commercial choices. They are signals — to governments, regulators, investors, customers, and competitors.

The companies that understand this shift will treat rare earths not as a narrow sourcing issue, but as a test of leadership. The companies that do not will keep discovering, usually too late, that supply chains are now instruments of state power.

Why Rare Earths Belong on the Executive Agenda

The 17 elements classified as rare earths are not, strictly speaking, rare. What is rare is the ability to extract, separate, refine, and process them economically, responsibly, and at scale. That distinction matters. Modern industry depends less on the existence of minerals in the ground than on the industrial systems that turn them into usable inputs.

Neodymium powers the permanent magnets used in electric vehicles and wind turbines. Dysprosium helps those magnets withstand high temperatures. Yttrium and erbium support fiber optic systems. Terbium is used in advanced defense applications. Rare earths and related high-performance materials are embedded in fighter jets, satellites, robotics, batteries, semiconductors, medical devices, telecommunications infrastructure, and clean energy systems.

These are not niche inputs. They are the material foundation of the clean energy transition, next-generation defense capability, and the digital economy. By 2040, the International Energy Agency expects demand for minerals used in clean energy technologies to rise sharply as electric vehicles, wind power, grid infrastructure, and energy storage scale.2 Demand from defense, AI infrastructure, advanced electronics, and aerospace will add further pressure.

The broader category of critical minerals matters just as much. Titanium, gallium, germanium, palladium, nickel, graphite, lithium, cobalt, uranium, and other materials are not all rare earths, but they sit in the same strategic universe. They are essential to aerospace, batteries, nuclear energy, semiconductors, defense systems, and industrial manufacturing.

The Russia-Ukraine war showed how quickly disruption in one mineral category can cascade across sectors. Nickel prices spiked after Russia’s invasion. Aerospace companies reassessed exposure to Russian titanium. Palladium supply became a concern for automotive and semiconductor manufacturers. The issue was not one mineral. It was the fragility of industrial systems built around concentrated and politically exposed inputs.3

For executives accustomed to treating rare earths as a line item in materials sourcing, the scale of this dependency can feel abstract. It is not. Companies whose strategies depend on electric vehicles, offshore wind, AI infrastructure, semiconductors, aerospace, batteries, telecommunications, or advanced manufacturing are making an implicit bet: that rare earth and critical minerals supply will remain accessible, affordable, compliant, and politically stable.

That bet deserves explicit board-level scrutiny.

The Concentration Problem Is Structural, Not Cyclical

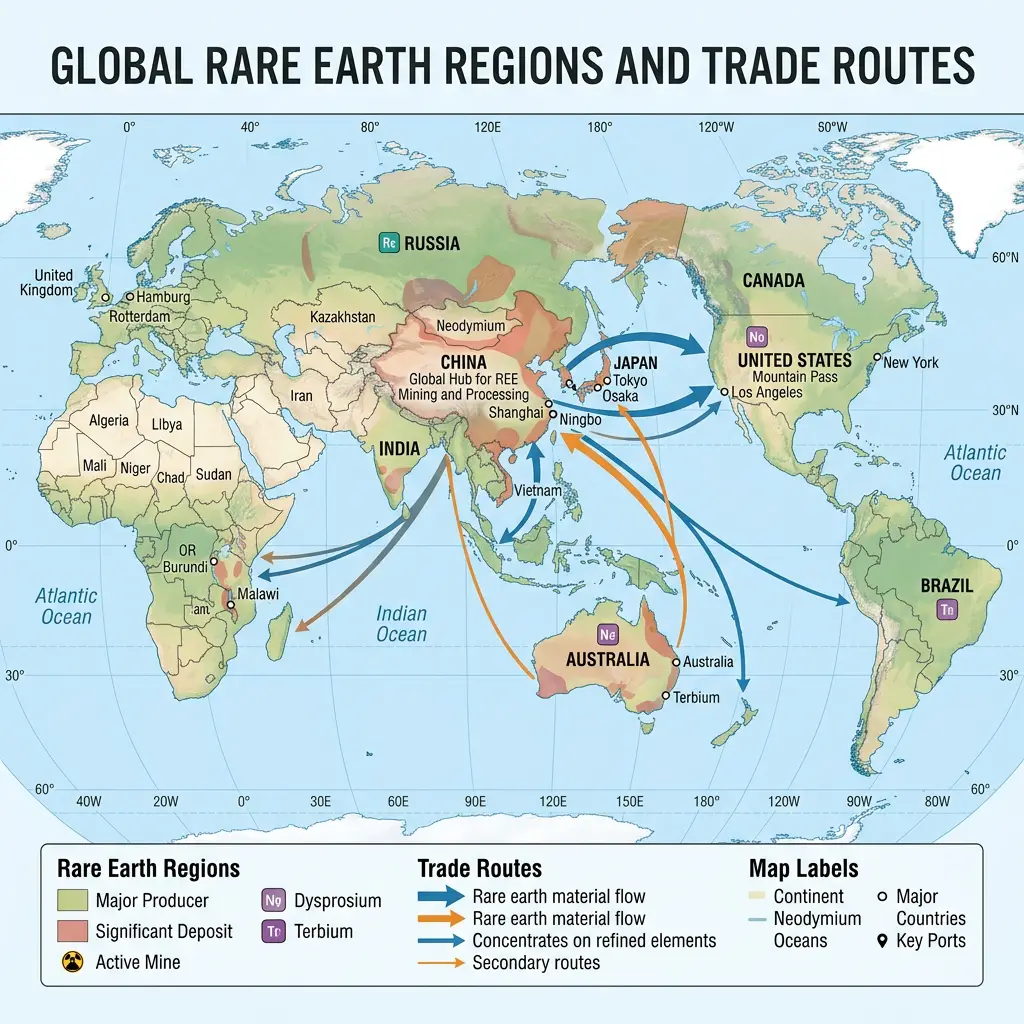

China controls the dominant share of global rare earth processing and a large share of production. This is not a temporary market imbalance that will self-correct as prices rise. It is the result of decades of industrial policy, infrastructure investment, technical expertise, and environmental tradeoffs that competitors cannot replicate quickly.

That is the first mistake many companies make. They treat concentration as a market defect. In reality, it is a strategic outcome.

The 2010 China-Japan episode established the modern template. During the Senkaku Islands dispute, China showed that rare earth dominance could be translated into geopolitical leverage.1 Since then, the pattern has widened.

China has also used export controls on adjacent critical minerals to send a broader signal. Restrictions on materials such as gallium and germanium, along with controls affecting graphite and other strategic inputs, demonstrate that Beijing views minerals policy as part of technology competition. For companies, the implication is uncomfortable but clear: supply chains that depend on Chinese-controlled processing are exposed not only to market cycles, but to political decisions.

Russia’s war in Ukraine reinforced the point from another direction. Russia is not the rare earth power China is, but it matters in several critical minerals and industrial inputs. After the 2022 invasion, Western governments and companies reassessed exposure to Russian nickel, palladium, aluminum, uranium, titanium, scandium, and other materials. Boeing suspended purchases of Russian titanium in 2022, while Airbus faced more complicated tradeoffs because of its continued reliance on Russian supply.3 Palladium markets tightened because Russia accounts for a significant share of global production. Nickel markets were rattled by fears of disruption.

The lesson was not simply about sanctions. It was about the wider ecosystem of risk. Even when a mineral is not directly sanctioned, banking restrictions, insurance limits, shipping risk, reputational pressure, and voluntary corporate disengagement can disrupt supply.

Ukraine adds another dimension. It is not only a battlefield; it is also a potential future node in allied critical minerals strategy. Ukraine has significant reserves and industrial history in titanium, lithium, graphite, uranium, gallium, zirconium, and other critical minerals. Many resources are underdeveloped. Some geological data is outdated. Some deposits are in or near conflict-affected areas. But the strategic logic is powerful: Ukraine’s reconstruction could become a test case for aligning security assistance, industrial policy, private capital, and critical minerals development.4

Iran presents a different kind of risk. It is not a major rare earth supplier in the way China is, and executives should not overstate its near-term role in rare earth markets. Its importance lies in the intersection of mineral potential, sanctions, nuclear tensions, regional conflict risk, and strategic alignment with China and Russia. Iran has significant mineral resources, including copper, zinc, iron ore, uranium, titanium-bearing minerals, and reported rare earth potential. But sanctions, investment constraints, and political risk limit its integration into Western supply chains.5

For companies, the key question is not whether Iran becomes a major rare earth supplier tomorrow. It is whether mineral diplomacy becomes part of a sanctions-evasion strategy, a regional influence strategy, or a China-aligned resource strategy that complicates Western access and compliance.

These cases share a common thread: critical minerals can become leverage in geopolitical disputes even when they are not the original cause of those disputes.

For companies operating across jurisdictions, the implications are direct. Working with Chinese suppliers may invite scrutiny in Washington and Brussels. Excluding them may create market access issues elsewhere. Engaging suppliers with Russian, Iranian, or sanctioned-party exposure may trigger compliance and reputational risk. There is no neutral position. Every supply chain choice is also a diplomatic choice, whether leaders acknowledge it or not.

Conflicts Are Rewriting the Minerals Map

The rare earth and critical minerals map is no longer determined by geology alone. It is being redrawn by conflict, sanctions, export controls, reconstruction finance, strategic partnerships, and infrastructure risk.

Ukraine is the clearest example. Its mineral endowment has become part of a broader conversation about economic security and postwar reconstruction. At a 2026 Council on Foreign Relations discussion, Ukrainian and U.S. officials described how Ukraine’s critical minerals sector could support reconstruction, attract private capital, and deepen economic ties with allies. They also identified major barriers: outdated geological mapping, damaged energy infrastructure, security risk, limited laboratory capacity, and the need for de-risking tools such as political risk insurance, offtake agreements, first-loss capital, and public development finance.4

That matters for corporate strategy. A company evaluating Ukraine cannot treat it as a conventional sourcing opportunity. It must assess security risk, infrastructure resilience, government relationships, allied financing, sanctions exposure, logistics, processing capacity, and the credibility of geological data. It must also consider whether participation in Ukraine’s critical minerals reconstruction could strengthen its standing with Western governments, investors, and customers.

Ukraine is not just a mining opportunity. It is a business diplomacy challenge.

Russia demonstrates the other side of the equation. The invasion of Ukraine forced Western governments to consider sanctions beyond energy and into the broader natural resources and manufacturing complex. Even where minerals were not fully sanctioned, companies faced disrupted access to financing, shipping, insurance, and reputational legitimacy. Firms had to ask not only, “Can we buy this?” but also, “Should we buy this — and what will regulators, investors, customers, and governments infer if we do?”3

Iran adds another layer of complexity. Sanctions have long constrained foreign investment in Iran’s mineral sector. But Iran’s strategic partnerships, including its long-term cooperation with China, raise questions about how mineral resources may support geopolitical alignment outside Western-led frameworks. If Iranian critical minerals development expands with Chinese financing or technology, Western companies may face a more fragmented sourcing landscape in which access, compliance, and political alignment are harder to separate.

Other flashpoints matter as well. Myanmar has been an important source of heavy rare earth feedstock used in Chinese processing, and conflict there has repeatedly raised concerns about supply reliability and human rights exposure. The Democratic Republic of Congo dominates cobalt mining, making battery supply chains vulnerable to political instability, labor concerns, and ESG scrutiny. The Red Sea security crisis has reminded companies that mineral supply chains depend not only on mines and refineries, but also on shipping lanes, ports, insurance markets, and military stability.

The pattern is unmistakable. Mineral supply risk is no longer a narrow sourcing question. It is a geopolitical systems problem.

Diversification Solves Geography. It Does Not Solve Geopolitics.

The standard corporate response to supply concentration is diversification. That is the right instinct. Australia’s Lynas Rare Earths, Canada’s Nechalacho project, U.S. efforts around Mountain Pass, and the EU’s Critical Raw Materials Act all represent meaningful progress toward a more distributed supply base.

But diversification solves only part of the problem. It addresses geography. It does not address governance.

A company can diversify away from China and still be exposed if its new suppliers operate in jurisdictions facing conflict, sanctions risk, weak infrastructure, environmental controversy, or regulatory instability. It can sign an offtake agreement and still lose access if export controls change, shipping routes close, or a supplier becomes politically unacceptable. It can secure supply and still fall short if it cannot prove responsible sourcing under emerging due diligence regimes.

The rare earth landscape is shaped by export controls, sanctions regimes, environmental due diligence requirements, defense procurement priorities, industrial subsidies, and critical minerals legislation that are being written and revised in capitals around the world. Companies that monitor these developments passively — waiting for rules to be finalized before adapting — are already behind.

The EU’s Critical Raw Materials Act, which entered into force in 2024, sets targets for domestic extraction, processing, and recycling and seeks to reduce excessive dependence on single third-country suppliers.6 Businesses that engaged early had an opportunity to help policymakers understand commercial realities, permitting barriers, financing gaps, and implementation timelines. Those that arrived late are now adapting to rules shaped by others.

The same pattern is visible in the United States. The revival of the Mountain Pass mine in California — the only active rare earth mine in the country — was not simply a market-driven event. It reflected sustained engagement among MP Materials, the Department of Defense, and federal policymakers who viewed domestic rare earth processing as a national security priority.7 Companies that helped make that argument and positioned themselves within the resulting framework gained partnerships, government support, and strategic advantage that procurement optimization alone could never have produced.

The lesson is consistent: policy shapes the market. Public affairs shapes the policy. And in conflict-exposed supply chains, government relations can determine whether a company gains access to capital, permits, partnerships, or political support.

Public Affairs Is Now a Supply Chain Function

If supply chain decisions are diplomatic decisions, then the function responsible for managing government relationships must sit closer to the center of corporate strategy. That function is public affairs and government relations. In many companies, it is still treated as a communications, reputation, or stakeholder-management function. That model is outdated.

In the rare earth era, public affairs is not simply about explaining the company’s position after decisions have been made. It is about helping the company understand the environment in which decisions are possible.

Effective public affairs now operates across four dimensions.

1. Proactive Policy Engagement

Public affairs should not wait for policy frameworks to be finalized. It should help shape them.

The Minerals Security Partnership, launched in 2022 by the United States and allied partners, reflects a growing recognition that critical minerals security requires coordinated public-private action.8 Companies that engage in these forums gain access to government networks, preferred sourcing relationships, financing pathways, and supply chain intelligence that commercial channels alone cannot provide.

This dynamic will continue as implementation rules under the EU Critical Raw Materials Act develop, as bilateral critical minerals agreements expand, as Ukraine reconstruction finance is structured, and as export-control frameworks governing U.S.-China technology competition evolve.

These are not closed processes. They are active negotiations. Industry voices with credible data, operational experience, and real investment commitments can shape outcomes.

2. Sanctions and Export-Control Foresight

Public affairs and government relations teams must also become early-warning systems for sanctions and export controls.

The Russia-Ukraine context showed that legal compliance is only the starting point. Even if a mineral or supplier is not directly sanctioned, banks, insurers, customers, investors, and governments may still treat the exposure as unacceptable. By the time that pressure becomes visible in procurement systems, strategic options may already be limited.

The same logic applies to Iran. A supplier may appear immaterial today, but a transaction touching Iranian entities, intermediaries, shipping networks, or Chinese-Iranian resource partnerships can create compliance and reputational risk. In an environment of intensifying sanctions enforcement, public affairs must work closely with legal, compliance, procurement, and strategy teams to map direct exposure and second- and third-order risk.

3. Operational Credibility as a Policy Asset

Credibility in policy engagement is not built through messaging. It is built through operational commitments that public affairs teams can translate into policy arguments and stakeholder trust.

Apple’s Daisy robotic recycling system is a useful example. Daisy disassembles iPhones and recovers valuable materials, including rare earth elements used in components. It is often described as an environmental initiative. It is also a public affairs asset.9

Because Apple has built tangible circular economy infrastructure, it can engage regulators developing e-waste standards, responsible sourcing rules, and recycling requirements from a position of credibility rather than compliance anxiety. When policymakers consider recycling mandates or sourcing disclosure rules, companies with real operating capability have a stronger voice. When investors ask how the company manages scarcity risk, there is an operational answer.

That position is not available to companies that have made only rhetorical commitments to sustainability.

4. Geopolitical Intelligence as a Leadership Function

Public affairs teams with real geopolitical expertise can identify emerging supply threats before they become operational disruptions.

The China-Iran cooperation agreement, Russia’s mineral export posture, Ukraine’s reconstruction financing, instability in Myanmar, and China’s use of export controls are not isolated news items. They are signals. Properly interpreted, they can help companies anticipate future supply constraints, regulatory scrutiny, and partnership opportunities.

Most public affairs functions are not staffed or structured to provide that intelligence. They should be. In the rare earth era, public affairs is not simply about maintaining relationships with government officials. It is about translating geopolitical change into board-level choices.

The Board Conversation That Is Not Happening

Ask most audit or risk committees how their company’s rare earth supply chain would hold up if China expanded its export restrictions, if a key alternative supplier faced sanctions, if a shipping route closed, or if allied-nation procurement preferences began to exclude companies without traceable sourcing.

In many cases, the honest answer would be: we do not know.

That is not a procurement failure. It is a governance failure.

Rare earth exposure belongs on the board’s strategic risk agenda alongside climate risk, regulatory risk, sanctions risk, cyber risk, and geopolitical risk. It should not be delegated entirely to a materials sourcing committee. It requires the same quality of scenario analysis, executive accountability, and board-level visibility as any other category of exposure that could materially affect a company’s ability to operate.

Boards should be asking:

- Which rare earths and critical minerals are essential to our products, infrastructure, or growth strategy?

- Where are those materials mined, processed, refined, and transported?

- Which suppliers have exposure to China, Russia, Iran, sanctioned entities, conflict zones, or high-risk jurisdictions?

- What happens if a supplier becomes unavailable for 90 days, six months, or two years?

- Which emerging regulations could change our access, disclosure obligations, or procurement eligibility?

- Do our public affairs and government relations teams have the expertise and mandate to shape the policy environment before rules are finalized?

- Can we prove that our sourcing practices match our public commitments on resilience, sustainability, and responsible business?

These are not technical procurement questions. They are questions of strategy, governance, and leadership.

Addressing the Counterargument

Some executives will resist this framing. Securing critical mineral supply, they will argue, is a matter of national policy. Companies should focus on operations and let trade negotiators, defense planners, and foreign ministries manage the geopolitical dimensions.

The instinct is understandable. It is also wrong.

Governments are acting. The Minerals Security Partnership, the EU Critical Raw Materials Act, U.S. Defense Production Act investments, Ukraine reconstruction initiatives, and domestic processing support all show that public leaders understand the stakes.

But governments do not build resilient supply chains alone. They act through private sector partnerships, procurement relationships, investment incentives, offtake agreements, and regulatory frameworks. Those frameworks are shaped by industry engagement.

Public policy in this space emerges from negotiation between public priorities and private capabilities. Companies that show up with serious proposals, credible investments, and a willingness to contribute to shared goals can influence the rules. Companies that stay out inherit rules designed by others.

Ukraine illustrates the point. Governments can provide political risk insurance, development finance, first-loss capital, and diplomatic support. But private companies must still build mines, processing facilities, logistics networks, recycling systems, and customer relationships.

Iran illustrates the opposite risk. When Western companies cannot or will not engage because of sanctions and political risk, other actors can fill the space. China illustrates the long-term strategic result when industrial policy, processing capability, and corporate alignment reinforce one another over decades.

The shape of critical minerals policy over the next decade will reflect the voices that participate in its formation. Most boards are not yet in that conversation. That is not a reason to stay out. It is the strongest argument for getting in.

What Strategic Maturity Looks Like

For senior leaders, the rare earth challenge requires practical shifts that go well beyond procurement.

Elevate rare earth and critical minerals risk to the board level. This is not a materials-management issue. It belongs alongside geopolitical risk, climate risk, sanctions risk, and regulatory risk on the board’s standing agenda. Boards should have visibility into direct and indirect exposure, including second- and third-tier suppliers, processing locations, shipping routes, and sanctioned-party risk.

Rebuild public affairs as a geopolitical intelligence function. Public affairs teams need professionals with geopolitical literacy, sanctions awareness, industrial policy expertise, and experience in multilateral engagement. Relationship management still matters, but it is no longer enough. The function must be able to brief the C-suite on what a Chinese export-control change, a Ukraine reconstruction agreement, an Iran sanctions development, or a new EU due diligence rule means for corporate strategy.

Engage policy processes as a principal, not a bystander. Companies should participate in consultations and partnerships related to the EU Critical Raw Materials Act, the Minerals Security Partnership, U.S. critical minerals programs, and allied reconstruction initiatives in Ukraine. They should arrive with data, investment plans, operating experience, and clear proposals — not generic advocacy.

Build resilience into contracts, not just supplier lists. Diversification should include offtake agreements, inventory strategies, recycling commitments, alternative processing capacity, political risk insurance, and contingency plans for export controls or sanctions. Companies should know what happens if a supplier becomes unavailable for 90 days, six months, or two years.

Align sourcing standards with the values your products claim to represent. For companies in clean energy, electric vehicles, aerospace, semiconductors, or advanced technology, the environmental and labor record of the supply chain is becoming a compliance requirement, not merely a reputational concern. Rare earth mining and processing in jurisdictions with weak oversight can create ecological damage, labor risk, and investor scrutiny. Companies investing now in transparent, ethical, and traceable sourcing practices are building compliance infrastructure that will become a competitive advantage as requirements tighten.

Treat recycling and substitution as strategic hedges. Recycling will not eliminate the need for mining. Substitution will not remove rare earth dependency overnight. But both can reduce exposure to geopolitical chokepoints. Companies that invest in circularity, materials innovation, and product redesign are not only improving sustainability. They are creating strategic options.

The Decision That Defines the Decade

The decisions that will define corporate positioning in the rare earth era are not five years away. They are being made now — in sourcing contracts, government engagement plans, public affairs staffing decisions, sanctions-risk reviews, recycling investments, and board conversations that either include rare earth exposure or ignore it.

Japan’s post-2010 investments in alternative supply, recycling, and government-backed partnerships remain a benchmark for sustained public-private response. Ukraine may become the next major test of whether allied governments and private capital can build critical minerals capacity in a conflict-affected but strategically important country. Russia has already shown how war and sanctions can disrupt mineral markets even when companies are not the direct target. Iran shows how mineral potential, sanctions, and strategic alignment can complicate future supply-chain choices. China continues to demonstrate that processing dominance and export controls are instruments of statecraft.

By 2040, demand for rare earths and related critical minerals will rise substantially. Defense modernization, grid expansion, AI hardware, satellite systems, and advanced manufacturing will add to that pressure. The rules governing access to these materials — which suppliers are acceptable, which jurisdictions are compliant, which companies have earned durable partnerships, and which firms are left exposed — are being written now.

The executives and boards that lead effectively in this environment will not be those with the most sophisticated procurement models alone. They will be those who understand that in a world where critical materials are instruments of state power, the ability to engage governments, shape policy, build coalitions, manage sanctions risk, and create operational credibility is a core business capability.

Rare earths are a leadership test. The question is whether your organization has positioned itself to pass it.

References and Endnotes

- Reuters, “China cuts rare earth export quotas, U.S. concerned,” December 28, 2010; see also Robert Johnston, “Supply of Critical Minerals Amid the Russia-Ukraine War and Possible Sanctions,” Columbia University Center on Global Energy Policy, April 19, 2022.

- International Energy Agency, “The Role of Critical Minerals in Clean Energy Transitions,” World Energy Outlook Special Report, 2021.

- Robert Johnston, “Supply of Critical Minerals Amid the Russia-Ukraine War and Possible Sanctions,” Columbia University Center on Global Energy Policy, April 19, 2022. The commentary discusses Russia’s role in nickel, aluminum, titanium, scandium, palladium, and other critical minerals, as well as sanctions and market risks following Russia’s invasion of Ukraine.

- Council on Foreign Relations, “Ukraine’s Critical Minerals: Aligning Capital, Security, and Reconstruction,” event transcript, April 14, 2026. The discussion addressed Ukraine’s critical minerals potential, reconstruction finance, U.S.-Ukraine investment mechanisms, geological mapping, processing constraints, and security risks.

- SFA (Oxford), “Iran | Critical Minerals and The Energy Transition,” accessed 2026. The source discusses Iran’s broader critical minerals position, sanctions context, energy resources, uranium relevance, and geopolitical constraints.

- European Union, Critical Raw Materials Act, entered into force 2024; European Commission materials on critical raw materials resilience, extraction, processing, recycling, and diversification targets.

- U.S. Department of Defense and MP Materials public materials on support for rare earth separation and processing capacity at Mountain Pass, California; see also U.S. government critical minerals supply-chain initiatives under the Defense Production Act.

- U.S. Department of State, “Minerals Security Partnership,” launched 2022, including allied efforts to support responsible critical minerals supply chains.

- Apple, “Environmental Progress Report” and public materials on Daisy, Apple’s robotic iPhone disassembly system designed to recover materials from end-of-life devices.

Discover more from Responsible Public Affairs

Subscribe to get the latest posts sent to your email.